The Satyam scandal of 2009 gave Indian corporate stakeholders a cataclysmic jolt. Ramalinga Raju, who was recently sentenced to seven years in jail, was the chairman of Satyam Computer Services who committed financial fraud to the tune of Rs. 7000 crore. Shockingly, the company’s auditors, PricewaterhouseCoopers, did not notice it. The scale of the scandal and the auditing firm’s neglect brought to light glaring loopholes in the regulatory and legal framework dealing with the directors and the auditors of companies. Eventually, it led to changes in the law.

Before Satyam

Before the scandal, the erstwhile Companies Act, 1956, the primary legislation dealing with the conduct of corporations in India, did not contain any provision for independent directors or impose any stringent obligations on auditors. The report of the Kumar Manglam Birla Committee in 1999 recommended improvements to the function and structure of the board of directors of a company and emphasised disclosures to shareholders. Clause 49 of SEBI’s Listing Agreement (applicable to listed companies only) became a reflection of these recommendations. In 2002, the Naresh Chandra Committee on corporate audit and governance, drawing from the Sarbanes-Oxley Act in the United States, suggested various reforms relating to the appointment of auditors, audit fee, and the certification of accounts. In 2003, the Narayana Murthy committee analysed the role of independent directors, related parties, and financial disclosures. Clause 49 was amended to incorporate its recommendations with respect to the requirement of independent directors on corporate boards and audit committees and the compulsory disclosures that listed companies had to make to its shareholders.

After Satyam

After the scandal, the Confederation of Indian Industries set up a task force to suggest reforms and the National Association of Software and Services Companies established a corporate governance and ethics committee headed by Narayana Murthy. The report of the latter addressed reforms relating to audit committees, shareholder rights, and whistleblower policy. SEBI’s committee on disclosure and accounting standards issued a discussion paper in 2009 to deliberate on (i) the voluntary adoption of international financial reporting standards; (ii) the appointment of chief financial officers by audit committees based on qualifications, experience, and background; and (iii) the rotation of auditors every five years so that familiarity does not lead to corporate malpractice and mismanagement. In 2010, SEBI amended the Listing Agreement to include the provision dealing with the appointment of a chief financial officer but it did not insist on the compulsory rotation of auditors.

In 2009, the Ministry of Corporate Affairs also released a set of voluntary guidelines for corporate governance, dealing with the independence of directors, the roles and responsibilities of audit committees and the boards of companies, whistleblower policies, the separation of the offices of the chairman and the CEO to ensure independence and a system of checks and balances, and various other provisions relating to directors such as their tenures, remuneration, evaluation, the issuance of a formal letter of appointment, and placing limits on the number of companies in which an individual can be a director.

A new company law – independent directors, accountable auditors, additional disclosures

India’s 2013 company law incorporated many provisions and reforms suggested by the various committees and organisations during the past decade. It clearly established the responsibility and accountability of independent directors and auditors. It provided for the compulsory rotation of auditors and audit firms. In fact, it even prescribed a statutory cooling off period of five years following one term as an auditor.

Under the Companies Act, 2013 (“the Act”), an auditor cannot perform non-audit services for the company and its holding and subsidiary companies. This provision seeks to ensure that there is no conflict of interest, which is likely to arise if an auditor performs several diverse functions for the same company such as accounting and investment consultancy services. Auditors also have the duty to report fraudulent acts noticed by them during the performance of their duties.

Ramalinga Raju

The new law also insisted on companies having independent directors, that is, directors who do not have a material or pecuniary relationship with a company. The requirement under Clause 49 of the Listing Agreement, which applied only to listed companies, would thus apply to many more companies. Independent directors have been prohibited from receiving stock options and are not entitled to receive remuneration for their services, except for reimbursement. At least one-third of the board of a company has to consist of independent directors. Even the audit committee has to feature a majority of independent directors. One independent director is required to be a member of the remuneration committee as well.

Additional disclosure norms such as the formal evaluation of the performance of the board of directors, filing returns with the Registrar of Companies with respect to any change in the shareholding positions of promoters and the top ten shareholders, were also mandated. After Satyam, aggrieved Satyam stakeholders in the United States were able to initiate class action suits against the company and its auditors for damages. The same remedy is now available to Indian stakeholders.

(Vera Shrivastav is an Associate at LegaLogic law firm and is a part time researcher and writer.)

At the outset, it is important to note that corporate governance primarily concerns itself with public companies. The balancing of profit making with public or shareholder interests assumes legislative importance where the public are substantially interested in a corporation or where the shareholders are greatly dispersed. Such companies are invariably listed companies, that is, their securities are available on specified markets for purchase by all members of the public.

The board as interlocutor

In our previous article here, we outlined the evolution and purpose of the board of directors (“BoD”). We understood how the BoD, placed between shareholders and the executive management, is primarily a tool to resolve agency problems that arise to shareholders because of the diversification of ownership and control. Briefly summarised, the agency problems of a corporation are threefold: (a) conflicts between shareholders and management, (b) conflicts between majority and minority shareholders, and (c) conflicts between the controllers (majority shareholders or the management) and other stakeholders (such as creditors, clients, and regulators).

The role of corporate governance and law is therefore to effectively manage these conflicts. The BoD makes high-level decisions and monitors the performance of the management. It acts as a key interlocutor in the process of effective monitoring and resolution of these agency problems. The structure and organisation of the BoD assumes importance in addressing these problems. Historically, the BoD has been composed of the representatives of controlling shareholders, executive management, and at times, non-executive persons (who were representatives of other stakeholders such as creditors), people of prominence, or people otherwise affiliated to the company. This mix, although representative of the corporation, does not by itself eliminate the possibility of the functioning of the BoD being captured by the controlling constituents, that is, the controlling shareholders or the executive management, whichever has greater control of the corporation either through ownership or decision-making. This may lead to the decisions of the BoD being challenged by stakeholders on account of conflict of interest. In these situations it is likely that such decisions will be invalidated by courts or under law as it is difficult for a BoD composed in such a manner to demonstrate independence of judgment in cases where conflict is alleged by the affected stakeholders.

The prescription of non-executive and independent decision-making

Globally, the modern composition mandate of the BoD prescribes a mix of constituents including shareholder representatives, executive directors, and non-executive and independent directors (“IDs”). This mix has its origins in the corporate jurisprudence of the United States and the United Kingdom, self-regulation by stock exchanges, and legislation. The prescription for non-executive and independent directors in the U.S. was formed as a response to judicial decisions that gave weight to the non-executive and independent character of decisions in evaluating the proper discharge of the fiduciary duties of the BoD in situations of conflict such as self-dealing transactions and takeovers and business reorganisations. Corporate and accounting scandals such as those related to Enron and Worldcom further brought the failure of proper BoD oversight and action under public scrutiny and led to the mandatory prescription under the Sarbanes-Oaxley Act, 2002 (“SoX”). In the U.K., the concept of board independence dates back to the establishment of committees studying corporate governance beginning with the Cadbury Committee Report, 1992 and culminating with the consolidated Combined Code on Corporate Governance, 2008. Thus, the need for board independence that we have discussed in the previous paragraph, rose sharply after various multinational corporate failures resulting mainly from poor executive decision making, non-compliance with good company practices, and the internal corruption that ultimately reflected inefficient and conflicted board oversight.

Board independence in India

In India, the Securities Exchange Board of India (“SEBI”) has spearheaded the adoption of board independence starting with the Kumar Mangalam Birla Report, 2000 which was followed by the Narayan Murthy Report, 2004. The mandatory prescription of board independence in the form of requiring a certain number of non-executive and independent directors was achieved via self-regulation in the form of Clause 49 of the listing agreement between the stock exchange and the companies. The Companies Act, 1956 was silent on the aspects of board independence and general directorial responsibilities.

Three influential figures in the development of the corporate governance regime in India – Ramalinga Raju, Kumar Mangalam Birla, and Narayana Murthy.

In the wake of corporate governance failures such as those involving Satyam, further reform has been brought in place by the Companies Act, 2013 (“Act”), which now provides a legislative mandate for board independence, prescribes duties and responsibilities for the BoD, and fixes accountability on the actions of the BoD.

Importantly, the Act is the first Indian legislation to require corporate governance in the form of board independence not only from listed companies but also on public companies that (a) have a paid-up share capital of at least ten crore rupees, (b) have a turnover of at least one hundred crore rupees, or (c) have in aggregate outstanding loans, debentures, and deposits exceeding fifty crore rupees. Under the Act, listed public companies have to have at least one-third of its BoD consisting of IDs and the public companies (meeting the aforementioned criteria) are required to have at least two IDs.

The comprehensive and exhaustive criteria of independence for an ‘independent director’ (Section 2(47) read with Section 149(6) of the Act), which were missing from the Companies Act, 1956 are objective as well as subjective. One objective qualification to be an independent director is that a person cannot have any interests, pecuniary or real, in the company or its affiliates or with the promoters, directly or indirectly. The criteria that one must be a ‘person of integrity’ and ‘possess relevant expertise and experience’ are, on the other hand, subjective. The criteria also takes care to prohibit service providers such as accountants and legal professionals who meet specified thresholds in the form of pecuniary or transactional relationships with the company. It may be noted here that the Act for the first time lays down limits on the number of directorships an individual may hold simultaneously, namely, twenty for private companies and ten for public companies.

The roles and responsibilities of the IDs are expressly incorporated in Schedule IV of the Act. The Act mandates that the IDs have to exercise their judgments to take fair decisions in the interest of the company and the stakeholders and evaluate whether the BoD and the other directors are taking decisions safeguarding the interests of all the stakeholders. There are also broad guidelines prescribed for the IDs like upholding ethical standards of integrity, acting objectively, devoting sufficient time to ensure balanced decision-making in order to fulfil their duties and obligations such as assisting the company in implementing the best corporate governance practices and even to moderating and arbitrating in the interest of the company in situations of conflict between the interests of the company and shareholders. The Act gives enhanced significance to the role of the IDs to ensure that the companies are encouraged to follow the best corporate governance practices. In this regard, Section 173(3) of the Act requires that if the IDs are absent from any board meeting, any decision that is taken in the meeting shall be final only after it is ratified by at least one independent director. This provision also ensures that the board doesn’t arbitrarily take decisions in the absence of the IDs.

Board independence will be merely symbolic without adequate access to data and information, in the absence of which, even an independent director cannot be expected to discharge his function of oversight and control effectively. In order to ensure that the IDs are provided with enough data and information related to the affairs of the company, the Act mandatorily requires the companies to form various committees like the nomination committee, the remuneration committee, and the audit committee. Provisions have been made to involve the IDs in the decision-making of these committees by providing for conditions such as a minimum number of IDs or an ID as chairman of a committee.

Code VII of the Schedule IV of the Act requires the IDs to convene at least one meeting in a year without the presence of non-IDs and members of management which is called a ‘separate meeting’. The objective of conducting a separate meeting is to allow the IDs to discuss and evaluate the performance of the company, its chairperson, and other directors. It also allows the IDs to assess the quality, quantity, and timeliness of the flow of information between the management of the company and the board of the company which is necessary for effective and reasonable performance of the duties by the BoD. However, the powers of evaluation are reciprocal. The entire board also has the power to evaluate the performance of the IDs and the decision of whether to extend or continue the terms of appointment of the IDs is taken on this basis.

The SEBI has also brought in amendments to board independence requirements under the Model Listing Agreement to align it with the Act and adopt “best practices on corporate governance”. The provisions of Section 149(3) of the Act have been replicated by the SEBI in Clause 49(II)(B) of the Listing Agreement. The listing agreement also provides a limit on the number of directorships that a person can undertake while serving as an independent director. A person cannot serve as an independent director in more than seven companies at a time and if a person serves as a whole time director in any listed company, then the limit on his directorship as an independent director in other companies comes down to three.

Balancing the wide arena of responsibilities and obligations imposed on the IDs under the Act and to ensure that the IDs are not fastened with the liability in the affairs of the company where there is no involvement on their part, the Act provides that IDs may not be held liable for an offence by the company unless it is established that they had knowledge of the act and consented or connived in its occurrence. The Act provides that the “knowledge” of the ID can be attributed through board processes, therefore the records of a board meeting such as the minutes are enough to establish that the ID had “knowledge” of the act leading to an offence by the company. Further, the Act also provides that the ID may not be held liable if it can be proved that he acted diligently. There have been various judgments from the Supreme Court and several high courts where the IDs have not been held liable in the affairs of day to day management of the company. The liability instead, has been fastened on the people who had been in-charge of the affairs of the company and were responsible for the actions taken on behalf of the company. (See, Central Bank of India v. Asian Global Ltd., (2010) 11 SCC 203, National Small Industries Corpn. Ltd. v. Harmeet Singh Paintal, (2010) 3 SCC 330)

The reader may also note that the Act ushers in significant provisions regarding the constitution of the BoD and functioning of directors of the company. In our next article we will study the duties of directors (including IDs) from a legislative and judicial perspective and its impact on board independence and liability. We will also examine certain provisions of the Act which fix specifically liability on executive management or the BoD.

(Jitender Tanikella is a corporate and tax lawyer with an advanced law degree from Columbia University. Anirudh Rastogi is a general corporate lawyer with an advanced law degree from Harvard University. They are part of Tanikella Rastogi Associates.)

References

– llan, Kraakman, Subramanian, Commentaries and Cases on the Law of Business Organization, (Wolters Kluwer, 2009) 3rd ed., at 98.

– Umakanth Varottil, “Evolution and effectiveness of independent directors in Indian corporate governance”, Hastings Business Law Journal, Summer 2010, Volume 6, Number 2, Page 281.

– Jay Dahya & John J. McConnell, “Board Composition, Corporate Performance, and the Cadbury Committee Recommendation” (2005), available at http://ssrn.com/abstract=687429

– Erik Berglof and Ernst Ludwig von Thadden, “The Changing Corporate Governance Paradigm: Implications for Transition and Developing Countries” (1999), available at http://ssrn.com/abstract=183708

– Cadbury Committee: FINANCIAL REPORTING COUNCIL, REPORT OF THE COMMITTEE ON THE FINANCIAL ASPECTS OF CORPORATE GOVERNANCE (1992) available at http://www.ecgi.org/codes/documents/cadbury.pdf.

– Financial Reporting Council, The Combined Code on Corporate Governance, Jun. 2008, available at http://www.frc.org.uk/CORPORATE/COMBINEDCODE.CFM

– Report of the Kumar Mangalam Birla Committee on Corporate Governance (Feb. 2000), available at http://www.sebi.gov.in/commreport/corpgov.html.

– Report of the SEBI Committee on Corporate Governance (Feb.2003), available at http://www.sebi.gov.in/commreport/corpgov.pdf.

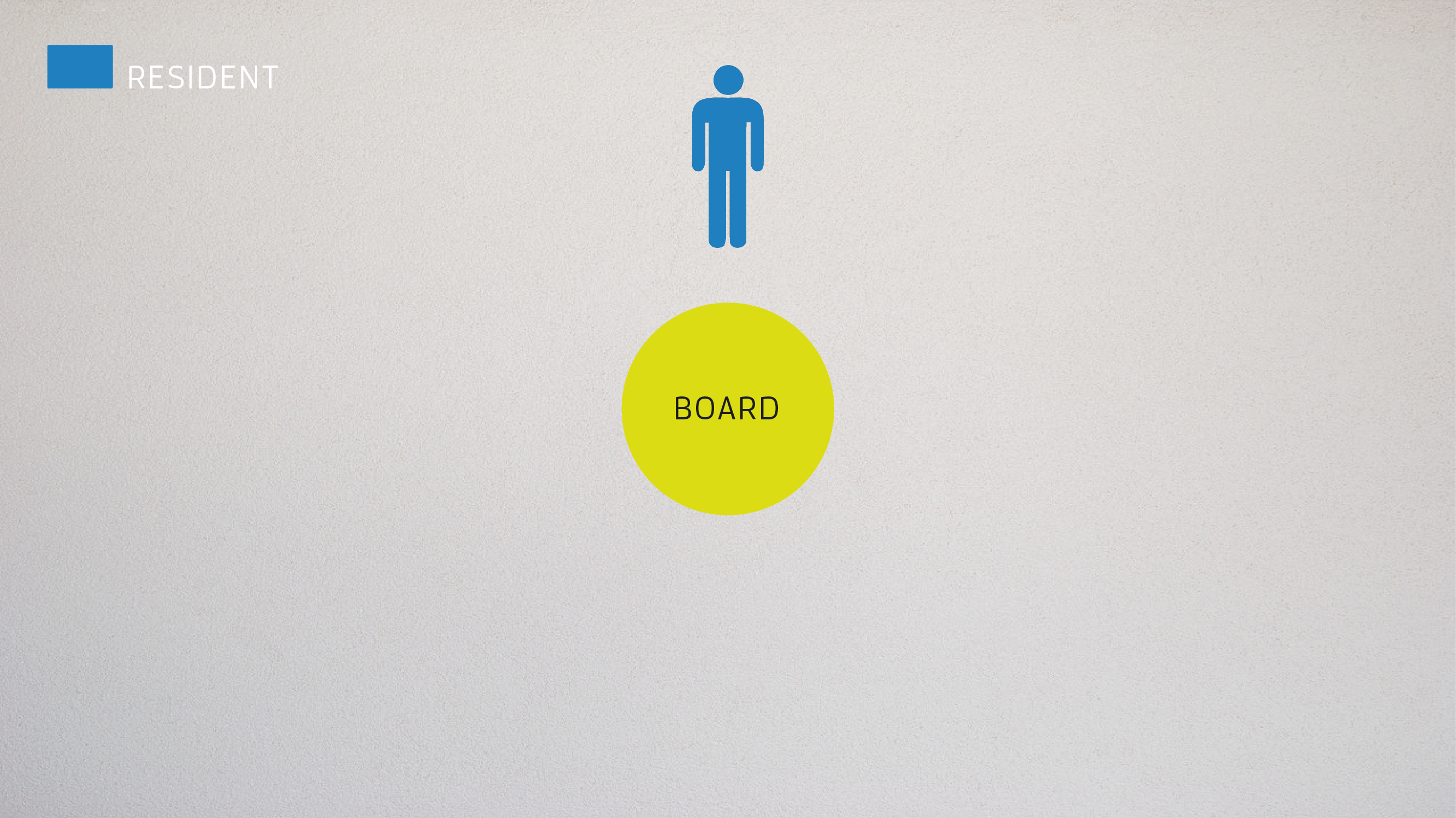

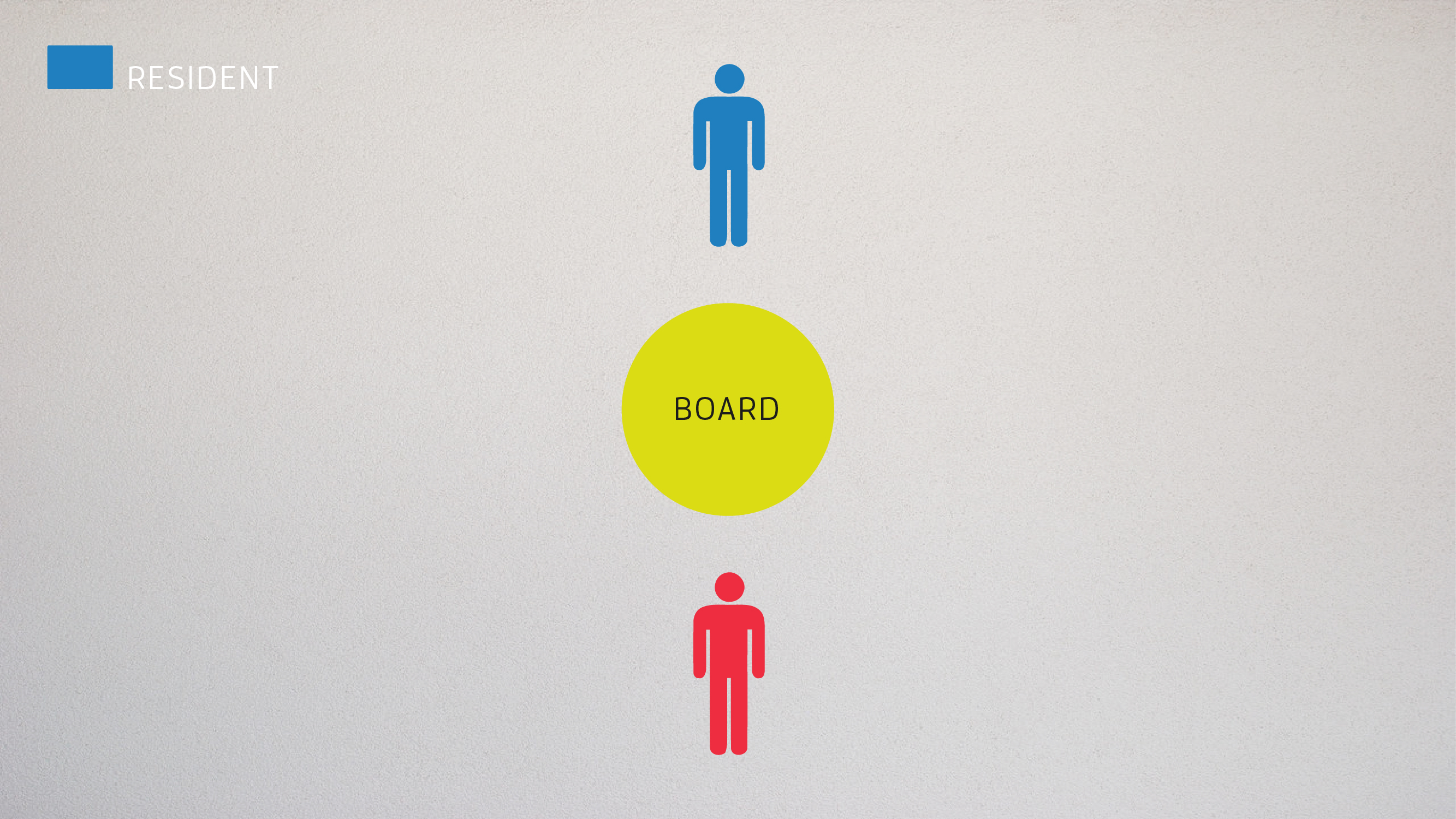

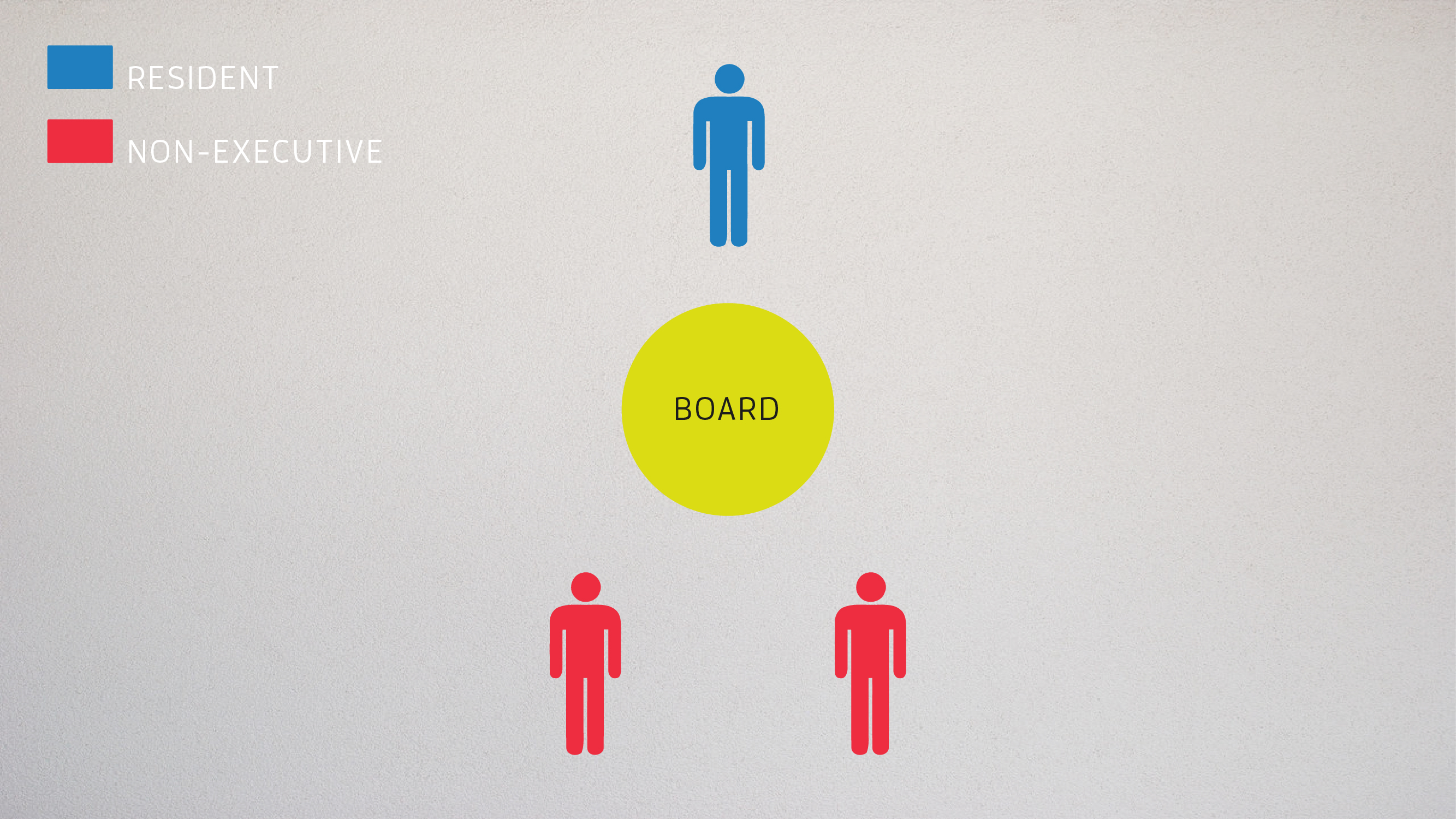

With the notification of the Companies Act, 2013 (“Act”) earlier this year, one of the most notable and much-discussed changes has been the focus on corporate governance. The key tools in this regard are the provisions relating to the composition of the Board of Directors (“Board”) of a company.

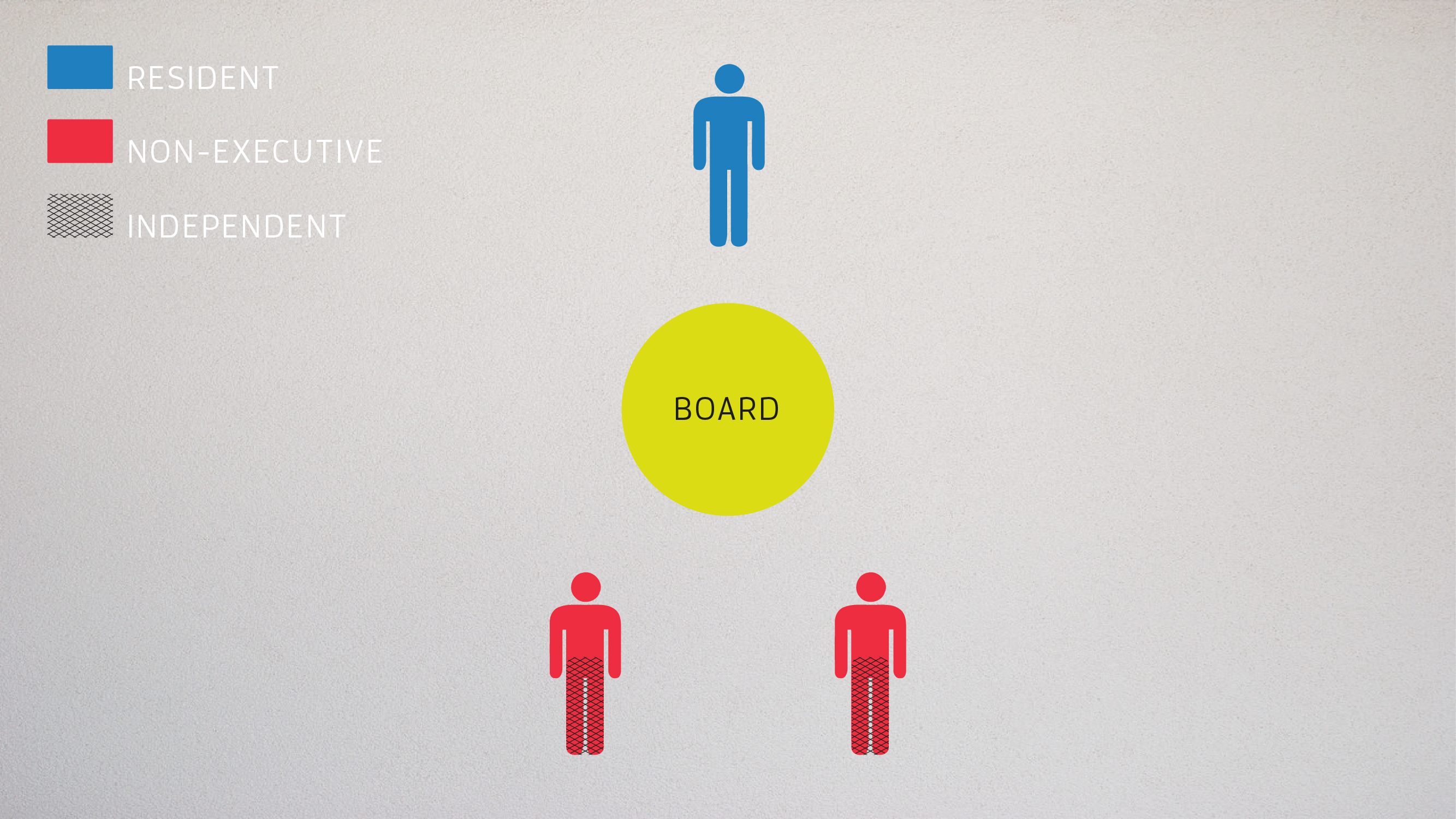

Let us now take a look at what the Boards of the following kinds of companies would look like if they met the bare minimum requirements in the Act, the Rules, and (where applicable) the Equity Listing Agreement.

One person company

Private company

Public unlisted company

Public listed company

Public listed company, where the Chairman is a non-regular, non-executive director or where the Chairman is a regular, non-executive director who is a promoter, or related to the promoter, or occupies a management position at the Board level in the company

Public company with a paid up share capital of Rupees Ten crore or more or with a turnover of Rupees One hundred crore or more

Public company with a paid up share capital of Rupees One hundred crore or more OR with a turnover of Rupees Three hundred crore or more

Public company with outstanding debt (loans, debentures, and deposits) of Rupees Fifty crore or more

Note 1: The charts above show the board having the minimum number of directors permitted for that category. Note that no company can have more than fifteen directors on its Board, unless a special resolution is passed to permit appointment of more directors.

Note 2: Where overlapping roles are shown for a particular director, it does not denote that the same person must necessarily fulfill both requirements (except that independent directors must be non-executive directors).

(Deeksha Singh is part of the faculty on myLaw.net.)

Continuing with our series of posts on the Companies Act, 2013 (“2013 Act”), let us now turn our attention to the role of independent directors in a company, an issue that has become increasingly important after the Enron and the Satyam scandals. As I will discuss below, India’s new company law has recognised independent directors as a vital facet in the operation of a company.

Independent directors are considered the watchdogs of a company. Appointed to the board of directors of a company to oversee its business, they should be free of all external influences. To ensure their complete autonomy, an independent director should not have any material or pecuniary relationship with the company.

Interestingly, the Companies Act, 1956did not contain any reference to independent directors. Further, the reference found in Clause 49 of the listing agreement is only applicable to listed companies.

Definition: The 2013 Act, for the first time, defines an “independent director”. Interestingly, the definition in Section 2(47) is similar to the one provided in theSEBI (Issue of Capital and Disclosure Requirements) Regulations, 2009, a regulation applicable only to listed companies. The principle of impartiality is embedded in this definition. An independent director can only be a person:

– who is not a managing director, whole-time director, or a nominee director;

– who is not or was not a promoter of the company or its holding, subsidiary, or associate company;

– who is not related to the promoters or the directors of the company, its holding, subsidiary, or associate company; and

– who has or had no pecuniary relationship with the company, its holding, subsidiary, or associate company, or their promoters, or directors, during the two immediately preceding financial years or during the current financial year.

Keeping in mind that an independent director must be free from all influence, the 2013 Act also places limits on the amount of shares that can be held in the company by a relative of such a director. Independent directors are also not entitled to any remuneration in the form of stock options.

Number of independent directors: Under Section 149 of the 2013 Act, there is a specific obligation on every listed public company that at least one-third of the board of directors should comprise of independent directors. This mirrors the requirement in Clause 49 of the listing agreement, and marks the first time that corporate governance norms have been recognised in company law in India. Additionally, Section 177(3) states that the majority of the members of an audit committee (in a listed company) must be comprised of independent directors.

In fact, Section 173(2) of the 2013 Act states that any board meeting held at shorter notice (to transact urgent business) requires the presence of at least one independent director. If such a director is not present, the matter discussed at the board will be considered approved only once an independent director ratifies it.

Protection from liability: Finally, in order to encourage a healthy environment where learned and well-respected individuals become independent directors in a company, the 2013 Act has, to a certain extent, protected independent directors from liability. Section 149 states that independent directors are liable only if any fraudulent act has been committed with the consent of such a director or where such director has not acted diligently and if such an act is attributable to the board process.

These are all welcome changes, and indeed, they will help improve the manner in which business is run in India by instilling strong corporate governance norms in a company.

(Deepa Mookerjee is part of the faculty on myLaw.net.)

After a long wait, the Rajya Sabha finally approved the Companies Bill, 2012 on August 8, 2013. The Lok Sabha had, after detailed deliberations, approved the Companies Bill in December 2012. It is now on the cusp of becoming an act, and only requires presidential assent and notification in the Gazette of India.

Once effective, it will replace a fifty-year-old legislation, the Companies Act, 1956 (“Companies Act”), the primary legislation for the incorporation, operation, and governance of corporate bodies in India. The bill promises to create a more effective, efficient, and simplified corporate law framework in India.

A good indication of the simplified structure is the overall framework of the Companies Bill. While the Companies Act consisted of 658 sections, the Companies Bill appears to be much cleaner, and takes only 470 clauses (divided into twenty-three chapters) and seven schedules to deliver the message. Through a series of posts here, I will explore and analyse the wide breadth of amendments proposed. To begin with, I will provide an overview of the major proposals.

One-person company

In line with global norms, the Companies Bill introduces the concept of “one person company”, a special type of private company. Defined in Clause 2(62) of the Companies Bill, the term simply means a company in which only one person is a member. These companies have been provided the flexibility of having only one director and enjoy exemptions in relation to filings and the holding of meetings. For instance, if there is only one director, Clause 122(4) of the Companies Bill proposes that a board resolution that needs to be passed can simply be entered in the minute books of the company, without holding a physical board meeting.

Private companies

Life may get tougher for private companies under the new regime. They stand to lose many of the exemptions they were entitled to under the Companies Act. A good example would be Clause 62 of the Companies Bill, which makes a special resolution a mandatory prerequisite for a preferential allotment in a private company. Under Section 81(1A) of the Companies Act, the requirement for a special resolution was applicable only to public companies.

Corporate Social Responsibility

Detailed provisions on corporate social responsibility (“CSR”) are also part of the Companies Bill. CSR activities have been made mandatory for the first time in India. Companies will have to spend on such activities in one financial year, at least two per cent of the average net profits of the three preceding financial years. This requirement is restricted, according to Clause 135 of the Companies Bill, to every company with: (a) a net worth of Rupees five hundred crore or more, or (b) a turnover of Rupees one thousand crore or more; or (c)a net profit of Rupees five crore or more, during any financial year. Such companies must constitute a corporate social responsibility board committee consisting of three or more directors, out of which at least one director will be an independent director.

M&A

Changes have been proposed in the procedure for mergers and amalgamations to make the process simpler and more efficient. The provision for fast-track mergers, where the approval of the National Company Law Tribunal is not required, if it is a merger between two small companies, between a holding and subsidiary company, or between any other companies as may be prescribed, appears to be a welcome change. Cross-border mergers have also been specifically permitted under the Companies Bill.

Corporate governance

The Satyam scandal has influenced the direction of Indian company law. Source: WIkimedia Commons.

In the wake of the Satyam scandal, the Companies Bill has sought to prescribe stringent standards of corporate governance. The term “independent director” has been defined, and the standards and qualifications necessary for appointment have been prescribed. Further, independent directors should make up at least two-thirds of the board of directors of every listed company. Interestingly, independent directors have been insulated from any liability in case of a fraudulent act (unless of course it has been done with their knowledge). It is expected that such a provision will go a long way in attracting the right kind of talent to these posts as they can now be assured that they will not be subject to any liability unless they have willfully taken part in it.

Class action suits

Clause 245 of the Companies Bill introduces the concept of class action suits. Simply put, a class action suit is one where a number of persons with the same claims and legal grounds can sue a corporate body. The Enron situation, where class actions suits were filed in the U.S. against Enron claiming millions in damages, is a well known example.

Under the Companies Bill, a class action suit can be filed against a company, its auditors, directors, or other concerned experts by a prescribed number of members or depositors if they are of the view that the affairs of the company are being carried out in a manner that is prejudicial to their interest. It will indeed be interesting to see how this provision plays out in the corporate sector.

These amendments are just a few of the many changes proposed in the new Companies Bill. This proposed law looks to alter the way businesses are run today to make them more efficient and profitable, but also socially conscious and accountable to their stakeholders.

Even though it is difficult to predict how all the proposed changes will interact with each other, the corporate world will finally see some changes to Indian company law to bring it in line with the changing economic environment.

(Deepa Mookerjee is a member of the faculty at myLaw.net.)

The Satyam scandal of 2009 gave Indian corporate stakeholders a cataclysmic jolt. Ramalinga Raju, who was recently sentenced to seven years in jail, was the chairman of Satyam Computer Services who committed financial fraud to the tune of Rs. 7000 crore. Shockingly, the company’s auditors, PricewaterhouseCoopers, did not notice it. The scale of the scandal and the auditing firm’s neglect brought to light glaring loopholes in the regulatory and legal framework dealing with the directors and the auditors of companies. Eventually, it led to changes in the law.

The Satyam scandal of 2009 gave Indian corporate stakeholders a cataclysmic jolt. Ramalinga Raju, who was recently sentenced to seven years in jail, was the chairman of Satyam Computer Services who committed financial fraud to the tune of Rs. 7000 crore. Shockingly, the company’s auditors, PricewaterhouseCoopers, did not notice it. The scale of the scandal and the auditing firm’s neglect brought to light glaring loopholes in the regulatory and legal framework dealing with the directors and the auditors of companies. Eventually, it led to changes in the law.