Recently, a three-judge bench of the Supreme Court, in the case of People’s Union for Civil Libertiesand Another v. Union of India, directed the Election Commission of India to include the “None Of The Above” (“NOTA”) button on electronic voting machines (“EVMs”).

Following the decisions of the Supreme Court of India in Union of India v. Association for Democratic Reforms (2002), People’s Union for Civil Liberties v. Union of India (2003), and Kuldip Nayar v. Union of India (2006), confusion prevailed about whether the right to vote was a statutory right, a constitutional right, or a fundamental right. Harmoniously constructing these decisions, the Court held that while the right to vote was a statutory one, the voter’s decision — once granted the right or freedom of voting — is a fundamental right under Article 19(1)(a). The petition under Article 32 was therefore maintainable.

The Court then ruled that the present system of voter abstention was unconstitutional and ultra vires Article 19(1)(a) and Section 79 of the Representation of People’s Act, 1951 as secrecy must be extended to the right not to vote as well. The Court then accepted the Election Commission’s suggestion that a NOTA button be included in all EVMS.

The Court also listed some countries that offer the NOTA option in elections. The table below captures some of the details after correcting some of the Court’s factual errors.

(Vasujith Ram is a student of The WB National University of Juridical Sciences. He can be contacted at vasujith94@gmail.com)

REITs were created in 1960 in the United States to give investors the opportunity to invest in the real estate sector, which is a high-yield sector, using liquid securities. This allowed them to access this sector in the same way that they would invest in other asset classes. There are different types of REITs, classified on the basis of their investment strategy.

The Draft Regulations envisage trusts registered with the SEBI that invest in real estate assets, being operated by a manager, appointed by the trustee. They can invest in properties directly or through special purpose vehicles, but only in assets based in India. The Draft Regulations also specify the manner in which the units by the REITs can be issued and listed. You can read more about the proposed structure and guidelines for the kind of REITs that SEBI will permit in India, here.

A reading of the Draft Regulations indicates that the SEBI has given due importance to transparency to ensure that investors can invest through these vehicles with a complete picture of the risks and rewards involved. However, even if it enacts these Draft Regulations, both Real Estate Investment Trusts (“REITs”) and investors will need to take into account some of the concerns plaguing the Indian real estate sector.

Foremost amongst these is the lack of clear title in most real estate transactions in India. Before investors can be brought in to invest in these real estate assets, REITs will need to ensure that sound due diligence is conducted on each of these assets.

Grading system?

A possible solution lies in the implementation of a grading system. The assets that form part of a REIT’s corpus must be mandatorily graded before it can issue and list units. This system should not only take care of the valuation of assets, but also be used to establish a clear and marketable title. These assets should only be deemed investment-grade if these stringent requirements are satisfied. Thus, while there will be no reduction of the obligation on investors to go through the disclosures carefully before investing, a grading system will help ensure that issues specific to the real estate sector in India are taken into account.

The SEBI will need to revise the Draft Regulations to provide mechanisms to account for issues specific to the real estate sector in India. The Draft Regulations are open for comments from the public till October 31, 2013.

(Deeksha Singh is part of the faculty on myLaw.net.)

The history of the presence of children in armed conflict is as old as human civilisation. From Ancient Greece to the Middle Ages in Western Europe, children as young as ten have been actively conscripted into armies. They have been present in armed conflict in three roles — as baggage, that is, as members of families that tagged along with armed forces on military campaigns; as providers of services to armed forces in various capacities such as cooks, charioteers, and servants; and lastly, as direct participants in hostilities. Whether participants in armed conflict or just suffering its effects, children are the victims.

Why are children drawn into armed conflicts? To start with, they are very obedient. They are docile and do not question orders. Fear induced by threats of abuse and physical and sexual intimidation works far is far more effective on young and impressionable minds. More disturbingly, child soldiers are often drugged to create dependency-induced obedience. Children also need less food. With modern lightweight weaponry, children can also be armed to the teeth and require far less training than adults. The most soul-wrenching aspect of this evil however, is that children do not have a developed sense of morality. Morality is a product of conditioning and development. Children deprived of circumstances that provide this very necessary moral compass can be moulded into ruthless killing machines, remorseless and empty of guilt. Using children in armed conflict is unfortunately, a very profitable exercise.

Image above is from Wikimedia Commons and has been published under a Free Art License.

Modern international law prohibits the presence of children in armed hostilities. Since the Second World War, humanitarian law and the law of armed conflict have evolved constantly to provide greater protection to the most vulnerable and most affected members of society during war.

Today, it is generally accepted that children are not to be recruited into armed forces for any reason. However, international law remains divided on the issue of who exactly a child is.

On one hand, the First Additional Protocol to the four Geneva Conventions of 1949, at Article 77 (2), applicable to international armed conflict states:

“The Parties to the conflict shall take all feasible measures in order that children who have not attained the age of fifteen years do not take a direct part in hostilities and, in particular, they shall refrain from recruiting them into their armed forces. In recruiting among those persons who have attained the age of fifteen years but who have not attained the age of eighteen years, the Parties to the conflict shall endeavour to give priority to those who are oldest.”

“Children who have not attained the age of fifteen years shall neither be recruited in the armed forces or groups nor allowed to take part in hostilities”.

These Protocols, read with the four Geneva Conventions, form the core of modern international humanitarian law.

Apart from humanitarian law, the prohibition on the conscription of children below the age of fifteen has also found distinct mention in international criminal law. The Rome Statute that governs the ICC, at Article 8(2)(b)(xxvi), regards “conscripting or enlisting children under the age of fifteen years into the national armed forces or using them to participate actively in hostilities” as a war crime.

The African Charter on the Rights and Welfare of the Child, at Article 2, on the other hand, unequivocally defines a child as “every human being below the age of 18”. At Article 22(2), it clearly mandates State Parties to ensure that children do not participate in armed hostilities. Further, children cannot be recruited into armed forces.

As is evident, international opinion is divided on the age at which children achieve majority. In spite of these differences however, it can be said that it is now a principle of customary international law that children must not be recruited into armed forces and must not be permitted to participate in hostilities – directly or indirectly.

A child in a rebel camp in the Central African Republic. Image above is from Wikimedia Commons and has been published under a CC BY-SA 2.0 license.

The past three years have seen a resurgence of public interest in the involvement of children in armed hostilities. On July 10, 2012, Thomas Lubanga Dyilo became the first person to be convicted by the International Criminal Court (“ICC”) for war crimes, crimes against humanity, and the conscription of child soldiers in armed conflict. He is serving the last eight years of his fourteen-year sentence.

Last year, a short film based on child soldiers and the hostilities in Uganda created ripples in the international online community. It brought to light Uganda’s Joseph Kony and his Lord’s Resistance Army.

In 2009, Human Rights Watch published its Global Report on the situation of child soldiers. You can read more about it here. Similarly, UNICEF publishes an annual Fact Sheet on the phenomenon, and tracks governmental response to the situation across the world. Interestingly, it is Burma (Myanmar) that seems to have the largest number of child soldiers – about 70,000 of them in its army of almost 350,000 members.

Most recently, the Appeals Chamber of the Special Court of Sierra Leone upheld the conviction of Charles Ghankay Taylor of Liberia on eleven counts of war crimes, crimes against humanity, and other violations of international law, including the use of child soldiers in armed conflict. Charles Taylor was one of the first leaders of armed forces in Africa to not only conscript children (mostly between the ages of five and seventeen) but to have dedicated armed Small Boys’ Units and Small Girls’ Units in his army.

Under international humanitarian law and international criminal law today, child soldiers are not seen as perpetrators of war crimes but as the victims of the most heinous of such crimes. While the international community debates the exact definition of a child, these young ones suffer in the midst of some horrific armed hostilities.

(Suhasini Rao-Kashyap is part of the faculty on myLaw.net.)

In what is being termed as an “investor friendly” move, the Securities and Exchange Board of India (“SEBI”), permitted put and call options in shareholders agreements through a notification dated October 3, 2013. It appears that it will help clear up some of the ambiguity regarding the validity of these options under Indian law.

Simply, a “call option” is a right but not an obligation to purchase shares at a specified price, on the happening of a specified event. Assume that there are two investors — A and B — in a joint venture company. A has a call option over twenty-six per cent shares held by B, which he can exercise once the foreign direct investment (“FDI”) cap is raised. This means that once the FDI cap is raised, A has a right to purchase twenty-six per cent shares from B. If A exercises this right, B cannot decline to sell the shares to A.

A “put option” on the other hand, is a right but not an obligation to sell shares upon the occurrence of a specified event at a specified price. Here, assume that A has a put option over twenty-six per cent of his own shares in the company. A can exercise this option once the company is insolvent. If the company declares insolvency, A can sell his shares to B. Once A exercises his put option, B cannot decline to purchase A’s shares.

Historically, put and call options, along with other rights such as pre-emption rights and right of first refusal have been the subject of much controversy in India.

Prohibition under company law

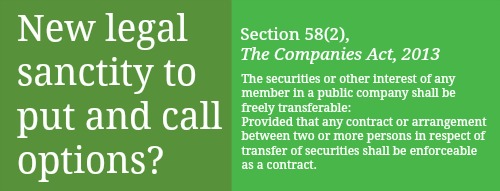

Section 111A of the Companies Act, 1956 stated that shares of all public companies were freely transferable. Hence, any restriction on the transfer of shares (including options in shares) would be illegal. Since, put options and call options restricted a person’s right to transfer shares, such options were illegal. Based on this, some market players took the view that even though these options were prohibited in a public company, private companies were free to incorporate such conditions.

This issue has been put to rest in the Companies Act, 2013, which states in the proviso to Section 58(2) that any contract or arrangement between two or more persons in respect of the transfer of shares will be enforceable. Though there has been no formal explanation for its insertion, one could argue that the proviso recognises shareholders’ competence to contract. It appears therefore, that this proviso lends legal sanctity to put and call options, which are essentially agreements for the transfer of shares between shareholders.

Prohibition under securities law

The Securities Contracts (Regulation) Act, 1956(“SCRA”) and the Securities and Exchange Board of India (“SEBI”) are the next set of roadblocks to these options. This is because, the SEBI had issued a notification in 2000, which provided that no person can enter into any contract for the sale or purchase of securities other than spot delivery contracts (Section 18, SCRA) or permissible contracts in derivatives. A “spot delivery” contract is one where the delivery and payment of shares takes place on the same or following day. (For a more detailed understanding of the development of the law, please look at Investment Agreements in India: Is there an “Option?”)

they were not valid derivative contracts that can only be traded on a stock exchange (Section 18A, SCRA); and

put or call options give parties the right to trade on shares at a future date which makes it an invalid “spot-delivery” contract under Section 2 (i) of the SCRA.

Contingent contracts and the Bombay High Court

Moreover, the Bombay High Court in Niskalp Investments held that a clause permitting the buy back of shares if certain conditions were not met would be hit by the restriction in relation to spot delivery contracts. Contingent contracts were also therefore, hit by prohibitions on spot delivery contracts. One can argue that call and put options are contingent contracts that come into effect once they are exercised. Once exercised, the delivery of shares and payment can take place simultaneously. These clauses therefore, are not invalid spot-delivery contracts. This position gained legal backing inMCX Exchange, where it was held that options come into existence only once the option is exercised. Till such exercise, the option is not fructified and therefore not hit by the prohibition. From all this, it was clear that there was much judicial debate on this issue. No clear answer was emerging.

In its recent notification, the SEBI has permitted options in shares and rescinded its 2000 notification. Put and call options are now permitted provided the seller owned the “underlying securities” for at least one year from the date of the contract, the transfer is priced according to existing laws, and the underlying securities are delivered. This puts the controversy to rest as far as SEBI is concerned, to a certain extent.

The RBI’s view

The Reserve Bank of India (“RBI”) had also expressed doubts on put and call options. It felt that granting put options to non-resident investors was akin to a debt investment made by such an investor. This is because an investment backed by a put option meant that the non-resident was guaranteed a specific rate of return. Such a transaction would therefore need to comply with the External Commercial Borrowing (“ECB”) Regulations. In fact, the Consolidated FDI Policy of October 1, 2011 contained a provision that stated that equity instruments issued or transferred to non-residents having in-built options or supported by options sold by third parties would lose their equity character and such instruments would have to comply with the extant ECB guidelines.

Interestingly however, this statement was later deleted from the policy by a notification issued by the Foreign Investment Promotion Board. This led to further confusion. Did the withdrawal mean that the RBI had implicitly permitted these transactions or that it was simply a withdrawal due to public pressure? The RBI has not clarified matters and this confusion still exists. Therefore, even though listed companies may get the go ahead from the SEBI, the RBI may still be a roadblock.

The Bombay High Court, the RBI, the SEBI, and the Ministry of Corporate Affairs have all made their views on put and call options heard.

To conclude therefore, the SEBI Notification has not put the controversy to rest. Since the SEBI Circular is only prospective, it only protects investments from October 3, 2013. Clarity is still required on the treatment of those arrangements entered into prior to October 3, 2013. Will those clauses be void?

Till these final issues are put to rest, the question mark still remains over the validity of put and call options.

(Deepa Mookerjee is part of the faculty on myLaw.net.)

Last week, Professor Nick Robinson wrote a well received op-ed in Mint, followed by a blog post on Law and Other Things, exploring Qui Tam enforcement as a possible solution to curb corruption in India. This post offers some more detail about the procedure.

Qui Tam is short for the Latin phrase, qui tam pro domino rege quam pro se ipso in hac parte sequitur, meaning “who pursues this action on our Lord the King’s behalf as well as his own”. A Qui Tam action allows a private citizen to sue on behalf of the government. Some part of the compensation or settlement money that is recovered if the suit is successful, is shared with the citizen while the majority goes back to the government. The idea is that a private citizen and the government work together to fight corruption and fraud.

English origins

Qui Tam is said to have been introduced in England in the fourteenth century to supplement an inefficient legal system. The early laws included many bounty provisions that rewarded citizens who successfully brought about civil and criminal actions on the King’s behalf. The procedure remained even after modernisation as it turned out to be valuable in bringing low-visibility cases or cases usually beyond detection before the courts. Though it stood for centuries, the English Parliament slowly strayed away from Qui Tam statutes in the nineteenth century and in the early twentieth till finally in 1951, with the passing of the Common Informers Act, 1951, all Qui Tam provisions were abolished.

False Claims Act

In the United States, Qui Tam action is usually taken under the False Claims Act(“FCA”), (31 USC §3729–3733). The FCA was passed during the U.S. Civil War to deter the corrupt actions of defence contractors. In 1943, during the Second World War, amendments weakened Qui Tam actions. They reduced the share of the private citizen and increased government powers to intervene. However in 1986, due to large scale fraud, especially in the defence sector, the FCA was again strengthened, to include greater penalties and a greater share of the recovery for citizens.

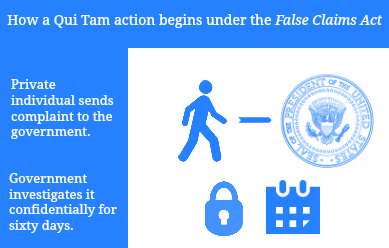

Under the law, a private individual has the locus standi to sue on behalf of the government against corrupt officials defrauding the government. In return, the private citizen would get upto thirty percent of the damages received in addition to the legal and other expenses incurred. If the government doesn’t join in the suit, the individual is entitled to an amount between twenty-five and thirty percent, whereas if the government intervenes in the suit, the individual gets between fifteen and twenty-five percent. While the government is the plaintiff, the private individual bringing out the suit is known as a “relator”.

It is important to note that under the FCA, the false claim need not be made directly to the government. The cause of action will arise even if the false claim is made to other parties, provided it ultimately causes a loss to the government. The complaint is actually served on the government, which keeps it under seal for sixty days and investigates the matter before deciding whether to intervene or not. The government can ask for an extension, and it has usually done so. The identity of the complainant is kept secret for the period that it is under seal but may be revealed at later stages of the suit.

This carries several risks for the complainant. During those sixty days, the private individual and his lawyer have to maintain strict secrecy. The question of personal involvement in the false claim may come up. If the complainant participated in the fraud in some manner, filing a Qui Tam action will not give that person any protection against being implicated by the government.

Constitutional and ethical risks

A constitutional objection rests on the doctrine of separation of powers. According to Article II of the U.S. Constitution, public law enforcement is the executive’s duty. How can a private individual be empowered to represent the polity in public interest? In India, it is important to note, the courts have relaxed the requirement of locus standi to a large extent in cases of public interest.

There are also ethical objections. Whistleblowing is morally justified by good motives. In Qui Tam actions however, the incentive is primarily financial. Since the motives are less altruistic, the potential whistleblower may withhold the complaint or action until the fraud has reached levels where it will generate greater financial gains in a suit. It even leaves scope for harassment and frivolous claims with mala fide intentions, purely out of opportunism. Individuals may even directly go for Qui Tam action without first trying to verify or redress it with appropriate authorities, internal or external. This risk is compounded because there is no requirement of direct knowledge of the fraudulent act.

Recovering billions

Even with its manifold problems, the Qui Tam action has been successful in retrieving billions of dollars. In 2009, pharma giant Pfizer settled for 2.3 billion dollars in a Qui Tam lawsuit against it for allegations that included illegal kickbacks and marketing fraud. More recently, in 2012, another pharma giant GlaxoSmithKline settled for three billion dollars, the largest Qui Tam settlement in U.S. history, after a suit was brought about defrauding government funded healthcare programs.

(Vasujith Ram is a student of The WB National University of Juridical Sciences. He can be contacted at vasujith94@gmail.com)

Recently, a three-judge bench of the Supreme Court, in the case of People’s Union for Civil Liberties and Another v. Union of India, directed the Election Commission of India to include the “None Of The Above” (“NOTA”) button on electronic voting machines (“EVMs”).

Recently, a three-judge bench of the Supreme Court, in the case of People’s Union for Civil Liberties and Another v. Union of India, directed the Election Commission of India to include the “None Of The Above” (“NOTA”) button on electronic voting machines (“EVMs”).